Leicester is the best city in the UK to invest in property and start a new business, a report by savings marketplace Raisin claimed.

The business survival rate in the city is over 91% and house prices have risen by 28.3% in the past two years,

The average house price in Leicester is £246,000, which has increased from £176,382 in the past two years – a rise of over £69,000.

Kevin Mountford, co-founder of Raisin UK, said: “Whether you’re buying a house, you have to weigh up the pros and cons, and the location is a key factor in that.

“Using the Raisin UK city investment index you can find the most practical and profitable location for your business and property needs, encouraging the most successful outcome of your investment and hard-earned savings.”

The second and third best cities were Bristol and Coventry, as both have high rates for business survival (88.7% and 90.6%) and house price increases of 26% & 28%.

Not only is it the start of a new year, but a new Decade, and in a few years time, we will look back at 2020 and realise that it was probably one of the best investing opportunities of this Decade. The question is, are you ready for 2020?

In this first article for 2020, I want to explain why this month (January) in particular is so important and why it will create a huge opportunity for you if you are ready for it. Unfortunately, many people will miss out on this opportunity and I don’t want that to be the case for you, so please make sure you read this article carefully to really understand the opportunity in front of you.

By the end of this month, everyone who is a landlord will need to have submitted their personal tax return for the 2018-19 tax year, and paid any tax that is due from the rental income on their property. This will be the second year that people will see and feel the affect of Section 24, which came into paly in April 2017. As I am sure you know, the Government decided that they wanted to change the way that property investors are taxed. What this means, is that if you own property in your own name (which most long term landlords do) and you are a higher rate tax payer (which most people in property are), then you will be paying more tax on your rental income. If your property is owned in a Ltd Company, instead of your own name, then you will not be effected by Section 24, and if you are a lower rate tax payer, then there is no impact, although some property investors will slip from a lower rate tax payer, to a higher rate tax payer, because of the way that rental profit is now calculated.

So what does this mean for you, and why is it the opportunity of the Decade?

Every month my organisation run 50+ local property investors network meetings all over the UK, and so I am I a unique position to have my ear to the ground in 50 locations around the UK to hear exactly what is going on with investors at a grass roots level. I can tell you for an absolute fact, that in 2019 we had far more long term landlord coming to our pin meetings than ever before because they are looking to sell some, or all of their portfolio, and retire early due to the impact that Section 24 will have on them and their income.

In any market you will also have new investors entering the market and some people retiring and exiting the market, but right now there are more landlords than ever thinking about selling up earlier than they have initially planned, because the don’t want ever decreasing return from their property portfolio.

January 2019 was the first time than many landlords realised the true impact of Section 24, when they saw the amount of tax they pay go up, and their accountant will have informed then that things are only going to get worse as the true effect of Section 24 is phased in over a 4-year period. January 2020 will be the second year that people see the effect of Section 24 starting to bite more into profits. This will be the catalyst for even more landlords to seek a solution to this problem and for some of those 1.75m landlords in the UK, I truly believe that early retirement may be the preferred choice for many of them, especially as they have seen tremendous capital growth over the last 10 years.

Whilst Section 24 is obviously very bad news for many landlords, there is always a silver lining in bad news, if you look close enough. For those property investors who want to expand their portfolio and acquire more property, 2020 will be a fantastic opportunity for a number of reasons.

First of all, we will see properties become available for purchase in previously locked down Article 4 areas. In these Article 4 areas, permitted development rights have been removed, so you have to get planning permission to convert a normal house into an HMO (with 3 or more unrelated tenants). However, if you do apply for planning in an Article 4 area, it will be automatically rejected because the local council does not want more HMOs. You can of course appeal and you might get planning permission if it meets all of the criteria, but it is very difficult. However, if you buy an existing HMO in an Article 4 Area, you don’t need to get planning permission. Instead you can just apply for a certificate of lawfulness as long as the property was used and an HMO before Article 4 was introduced in that area and has been continuously used as an HMO. Prior to the introduction of Section 24, in Article 4 Areas, landlords were quite happy keeping their property, knowing that there would not be too much new completion. But now some of these landlords are now considering selling which means that you can get access into theses effectively locked down areas.

The main reason why 2020 will be such a great time to acquire more property is because of the way in which you will be able to add to your cash flow and property portfolio. You see these landlords who decide to retire earlier than planned, have another problem. The main problem is that if they sell all of their properties in one go, they will have to pay a lot of Capital Gains Tax (CGT) on the profit from the sale. The best solution for anyone wanting to sell a number of properties, is to phase the sale over a number of years so that they can claim their personal CGT allowance and so reduce the amount of tax they will pay. But this creates another problem. The landlord will have to hang around until they sell their last property which in fact maybe they would rather be sat on a beach instead enjoying their retirement.

The good news for you, is that there a solution which you can provide these landlords so that they get to sell all of their property over a number of years, minimise the tax, and not have to hang around until the last one is sold. They can do this with the help of an investor like you, who can use Purchase Lease Options (PLOs) to take over the properties and manage them for the owners, with a schedule to buy them over a number of years. This means you get cash flow and potential equity growth on property that you don’t own, whilst providing a fantastic solution to these retiring landlords. You don’t need to have large desposits, or even be able to get mortgages to do this.

The only problem here is the PLOs are a massively misunderstand strategy. Most people who think they know about PLOs, don’t really know about PLOs otherwise they would have does a lot more of them by now. One of the main problems here is that PLOs only work in certain circumstances, namely when the seller does not need the money now and they have what we call favourable mortgage conditions. Luckily for you Landlords normally meet both of these criteria, which is why the strategy works so well for them.

Just in case you don’t know let me give you the basics about PLOs. This is where you enter into a legally binding agreement with a property owner, whereby you have the right (but not the obligation) to purchase their property, for a fixed price (The Option Price) agreed upfront, within a certain time period (The Option Period), and in the meantime you pay them a monthly payment (Monthly Option Fee), for which you are entitled to use the property. There is also a consideration (Upfront Option fee) required to make this a legally binding agreement. This upfront fee can be anything from as little as £1, but can also be several thousand pounds in some circumstances. During the Option Period you look after the property as if it were your own, and take care of all of the maintenance. For example, you might have the right to buy a property, for the current market value of £200k, anytime within the the next 5 years. In the meantime, you pay the owner a guaranteed £600 per month, and take care of all the bills, repairs and maintenance. You could then rent this property out in a way to generate a much higher income, such as an HMO or Serviced Accommodation, and you make a profit on the different between the rent you pay to the owner and the rent you achieve, less all the bills. This is cash flow for a property that you don’t own.

The main benefit for you as the investor, is that you don’t need to put down the typical 25% deposit that you would need if you actually purchased the property. You don’t need to get a mortgage on the property, because you don’t actually own it. You can benefit from positive cash flow during the option period and potential capital grow of the property over the option period. If you value of the property rises from say £200k now, to £250k in five years time, you have the right to purchase it if you want, at the agreed option price of £200k even though it is worth £250k.

How do you find these landlords? Well you can always attend your local property investors network (pin) meeting and ask for referral of landlords who may want to retire, or you can write direct to landlords using your local council list of licensed HMO owners.

I do hop you can see the incredible opportunity you have right now by helping these retiring landlords finding a win win solution

Invest with knowledge, invest with skill

By Simon Zutshi, Author of Property magic and Founder of property investors network

When the Alternative Credit Council recently predicted that the global private debt market will be worth in excess of $1 trillion by the end of 2020, some might have called the claim a little audacious.

Only seven years ago, less than £1 in every £10 lent in the UK came from an alternative lender.

Today, alternative lenders account for more than a quarter of the total UK lending market. It isn’t a fad, it is the new status quo.

A summer survey of over 550 European institutional investors said that private debt would be one of their favoured investment asset classes in the next three years. The conditions for alternative credit’s growth in the UK property market specifically couldn’t have been better.

It has come at a time when property finance from mainstream or high street banks is severely restricted. The banks that provided loans before 2008 have only returned to narrow parts of the property finance market, and with less than convincing enthusiasm. Cue thousands of creditworthy small and medium-sized property investment and development companies struggling to source the finance they need to finance their assets and grow their businesses.

Add to that the sheer volume of outstanding loans that are due to mature and will require refinancing.

Take, for instance, the commercial real estate market. In Europe alone, there are an estimated €500bn of loans due to refinance in the next four years. Without the traditional lenders there to offer new loans, alternative lenders have a big gap to fill.

But it’s the surge in interest from a widening global pool of investors that’s putting this alternative investment option so firmly on the map.

The appetite from institutions like pension funds and insurers has ramped up exponentially. One of the UK’s largest pension funds, RPMI Railpen, announced this summer that it is boosting its direct lending allocation (on behalf of its 350,000 UK railway industry pension holders) to as much as £4bn.

The constant hunt for yield is, unsurprisingly, a predominant driver to private debt. In this lower-for-longer interest rate environment, the search for income is a perennial preoccupation for investors. Plus, with equities at high valuations, new equity issues underperforming, and bond yields hitting historic lows, private debt has become the light at the end of the tunnel for yield-hungry allocators.

But what, beyond yield, is putting property debt investment so firmly on the radar of our pension funds and insurers?

Simply put, property equity investments are not as attractive as they once were. We’re observing a marked shift among investors from direct property equity investments to the private debt route.

As this extended economic cycle continues, the capacity for growth in property investments is tailing off. Furthermore, with yields in most sectors at all-time lows and rental growth prospects for the residential and commercial sectors also being relatively limited (according to the Office for National Statistics, rents grew by just 1.3 per cent in the year to October, while CBRE reports that commercial rents are flat), the outlook for returns from property is modest.

When these are compared with the returns generated by property debt positions, property debt investment looks really attractive on a risk-adjusted basis.

Pension funds and insurers are also influenced by how short-term property debt investing can be, adding greater liquidity to their portfolios.

Your traditional direct property equity position might last as long as a decade to defend against cyclical downturns in capital values and to offset high transaction costs. Even in institutional property investment funds, the minimum hold will be for no less than seven years. But shorter-term direct lending permits more flexibility; investors recoup their capital and recycle it sooner as opportunities and markets evolve.

Perhaps the most impactful — and exciting — driver is what institutional investors like about direct lenders’ evolving models.

The faceless bank mortgage or the transactional approach of a hedge fund or private equity lender are fast losing favour. Direct lenders and property finance borrowers are striking up a new, more sustainable way of working: a more specialist, relationship-managed experience that complements both parties’ goals.

Borrowers get finance on terms that work for them, and direct lenders achieve astonishingly high repeat borrower rates and lower than average arrears rates: testaments to a formula of lending that really works, and provides confident signals to investors that the credit quality is high.

However, we’re not there yet. Dutch non-bank lenders have been shaking up their mortgage market for years, and the Netherlands is home to myriad tales of how direct lending has transformed institutional investing.

But at a time when every investment decision counts, it’s encouraging to see the diversification and ambition of UK pension managers to try the alternative. More often than not, it’s better than the norm.

London continued to attract more foreign direct investment than any other UK city last year, prompting calls for a wider distribution of funds across the country.

The capital attracted 73 per cent of the total 624 projects secured in 2018, according to research by EY and the Centre for Towns.

The level of investment into the UK’s 12 largest cities has increased from 31 per cent in 1997 to 59 per cent in 2007, with London dominating the list.

However, Edinburgh, Leeds, Manchester and Newcastle upon Tyne more than doubling the number of FDI projects in the ten-year period.

The called for more investment in the UK’s towns and rural communities after research found that manufacturing FDI projects in former industrial and university towns fell by 50 per cent last year.

Over the last 20 years, large towns – with a population of more than 75,000 people – have seen their share fall from 26 per cent to 17 per cent.

EY chief economist Mark Gregory said: “The towns and conurbations on the periphery of the UK’s core cities are facing unprecedented economic challenges, but what is particularly worrying is how deep the economic disparity between cities, towns and smaller communities has become over the last 12 months.

“Core cities have been far more successful in attracting FDI while levels of investment in other locations has at best flatlined over the past 20 years.

“UK economic policy has tended to be based around core cities and this is likely to have exacerbated the geographic disparities in attracting FDI. With Brexit being one of a range of challenges facing the UK economy it is vital that a new approach to FDI policy, centred on geography, is developed as a priority.”

In total, 34 per cent of foreign investors said the availability of transport and technological infrastructure was an important factor when choosing a location to invest, while 32 per cent said the local skills base was a key criteria.

The UK has retained its position as one of the world’s leading hubs for business, according to a new report which suggest investors have taken a ‘wait-and-see’ approach towards Brexit.

In a comprehensive global index released this morning, the UK was ranked as one of the best global hubs for business, scoring highly for its low start-up costs and attractiveness for foreign investment.

Business advisory group Eight Advisory, which produced the report, suggested the long-term cost of Brexit has yet to emerge across a wide range of economic and wellbeing indicators.

“While Brexit creates considerable uncertainty the foundations of the UK’s economy are particularly strong, and it remains an attractive place to invest and do business,” said Alexis Karklins-Marchay, a partner at Eight Advisory and prominent figure within the French business community.

He told City A.M.: “Confidence has plummeted in the last 3 years, but Britain should have confidence in its own ability. This is one of the most competitive countries.”

Despite scoring highly in areas such as human freedom, higher education and happiness levels, the UK’s productivity was found to be “an ongoing and long-running concern”.

Eight Advisory also said that Brexit was proving a “distraction from the issues facing the UK economy”, such as productivity and standards of primary education.

The report comes weeks after consultancy Z/Yen showed that London has clung onto its second place in a ranking of the world’s top financial centres, but its position in the top tier is under threat amid Brexit chaos and other geopolitical shifts.

“There are fundamental issues that need to be addressed if the UK’s hard-earned reputation as an international leader is to be protected in the long term,” Karklins-Marchay added.

In spite of the Brexit cloud hovering over the British Isles, the UK economy itself has proven surprisingly resilient.

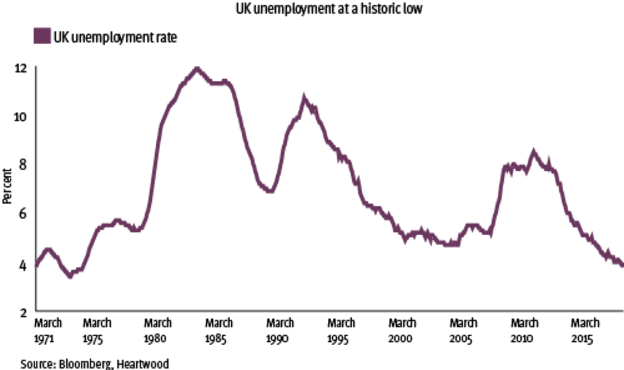

Low unemployment, a pick-up in wage growth relative to inflation, and expansion in the dominant services sector would all normally be welcomed by investors. Should we view the UK as an attractive place to invest, despite its political woes?

At around 4 per cent, UK unemployment is brushing up against historical lows, and faring much better in this regard than its European counterparts, with the exception of Germany.

Indeed, the UK’s latest jobs market data demonstrated the lowest unemployment rate since the 1970s, at 3.8 per cent.

Meanwhile, on mainland Europe, unemployment in France, Italy and Spain is around 9 per cent, 10 per cent and 15 per cent respectively – although these countries do usually have structurally higher levels of unemployment than the UK.

Key points

UK unemployment is at historic lows

In the corporate sector, confidence has stagnated

Brexit and political turmoil has stalled capital spending plans

Typically, with lower unemployment comes upward pressure on wages, which we are witnessing in the UK today.

In the three-month period to the end of May 2019, total earnings (not including bonuses) rose by 3.6 per cent – the highest since mid-2008.

Low and stable inflation is allowing this wage growth to translate into rising disposable incomes and increased spending power for British consumers – further good news for the economy.

Against this favourable labour market backdrop, UK interest rates have remained benignly low, and are likely to stay that way for the foreseeable future.

We believe that the Bank of England is ultimately looking to increase its store of dry powder in advance of any future recession – that is, raising interest rates so that it has room to cut them again in periods of economic weakness. For now, paralysed under a weight of Brexit uncertainty, it has little choice but to remain on the sidelines.

Over the longer term, we anticipate only gradual and minimal interest rate increases, particularly given the levels of debt in the economy.

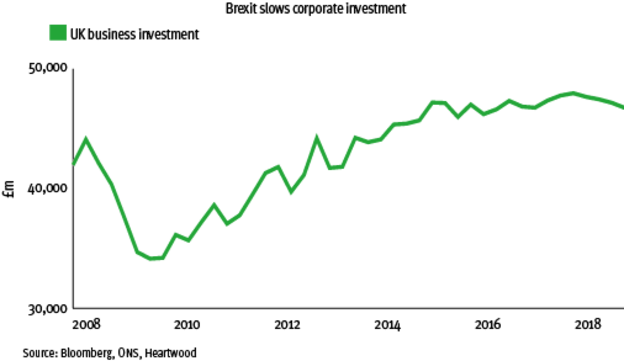

In the corporate sector, confidence and investment have both stagnated – typically a bad sign for economic growth – and more recently this has been evidenced in weaker economic data. However, rather than invest, UK businesses are currently stockpiling high levels of cash.

These excess corporate savings, held tight by nervous businesses, could be released if a Brexit resolution materialises. In turn, this could offer a potentially significant investment boost to the UK economy.

Nonetheless, the outlook for the UK economy is troubled, not least by a lack of clarity on Brexit, as well as the entwined domestic political turmoil.

This week, Conservative party members chose their next party leader, and by extension the new prime minister.

Shortly after, the UK will be back to the negotiating table with the EU, which has previously made clear that it has no intention of reopening the withdrawal agreement. However, a change of leadership in the UK and at the top of key EU institutions may just provide fresh impetus to the discussions.

Given the deeply uncertain political backdrop, the ‘wait and see’ attitude currently being adopted by investors is entirely understandable, as is the mirroring of this unease in the corporate world.

It is worth noting that while businesses stockpiling their cash could well mean a boost to the economy in the future, in today’s terms this means that growth in corporate investment has stalled.

Prolonged uncertainty surrounding Brexit could delay capital spending plans further, without the guarantee that these funds will be released into the economy in the future.

The UK’s dominant economic sector, services, is still in expansionary territory, which is encouraging.

However, in keeping with the global growth picture and concerns around global trade, the UK’s manufacturing sector, albeit much smaller than its services sector, is more troubled, with the latest business surveys showing that it is in contraction.

Further, there are key pockets of weakness in both the retail and real estate sectors, both of which faced an especially challenging 2018.

In addition, the UK has some notable structural problems. Perhaps most conspicuously, it has yet to deal effectively with its debt issues. The UK still sports twin deficits, meaning that the government spends more than it earns (fiscal deficit) and the country imports more than it exports (trade deficit), making it a net borrower overall.

In spite of its challenges, the UK has remained economically robust, and in the future could become an attractive place to invest once more.

The limited political will for a no-deal Brexit outcome is indeed a positive sign for domestically-focused UK assets and the potential for sterling strength ahead.

Nevertheless, UK shares remain markedly unloved by investors, and as a result they are also relatively cheap, appearing good value by virtually all measures, but particularly on price-to-book ratios (the total value of a company’s shares versus the value of its net assets).

Given its out-of-favour status, any change in sentiment could see large capital inflows to the UK stock market and provide a boost to valuations.

However, this simply cannot occur until we have more clarity in UK politics. Without this, and a more certain understanding of our future relationship with Europe, it is hard to justify significant further investment in the UK market in the near term.

For many investors, the finite nature of land translates into making property a safe, steady investment that diversifies a portfolio.

As ever in life though, if only it were so simple as just buying the asset – whether that is a building, an aircraft or a bond.

It’s not just what you buy that matters, it also matters how you buy it. This is especially true of property.

While a long-term, stable play, real estate is an illiquid asset. That means that you have to invest into it in a way that doesn’t lead you exposed to this fundamental fact.

The debacle around Neil Woodford’s Equity Income fund has highlighted how open-ended funds are not best suited to hold such illiquid assets. Open-ended funds by their very nature imply a promise of liquidity through redemption mechanisms funded by cash reserves or asset sales.

Despite the fine print warning of the possibility of “gating” and delays on redemptions, this is not what investors want or expect. If a fund suspends, as has happened with Woodford’s, it’s bad news for end-investors who find their money locked in when they did not expect it.

Ultimately, that doesn’t help anyone. Now the Bank of England is considering banning investors pulling their money out of open-ended funds at short notice if the underlying asset is hard to sell (of course, this includes real estate).

But while I would argue an illiquid asset like property is fundamentally mismatched to open-ended funds in their current guise, this shouldn’t take away from the fact that – when invested in the correct manner – property is a great investment.

Closed-end funds and co-investing are two investment structures much better suited to real estate, because they are not as fundamentally exposed to its illiquid nature.

As global macro uncertainty inches up, real estate is a solid play which investors will want it as part of their portfolio.

One of the prime real estate investment opportunities can be found in the UK’s build-to-rent (BTR) sector, which is far past the stage where it should be labelled as a niche or alternative asset class. It is accelerating into the mainstream, with investment predicted to reach £75bn by 2025.

That surge of investment is being driven by crystal clear market fundamentals.

The UK’s housing supply-demand imbalance has lasted for years, and will likely persist for decades given the past shortfalls in providing new housing.

However, the success of build-to-rent isn’t just down to a lack of homes, it’s about quality as well.

Renting through non-professional landlords remains a mixed experience for many, with the hassles of bills or having basic maintenance arranged often leaving many frustrated.

The sector is not just a London phenomenon – it is a solution that is being applied nationwide.

For regional cities, towns, businesses, and workers alike, this is good news. Build-to-rent can accelerate the supply of homes in regions, encouraging workers to move around more and help businesses outside of the capital attract top class talent.

Our partnership with Moda Living is primed to capitalise on this, with 6,500 apartments in key cities across England and Scotland.

Of course, any discussions about investing into the UK at the moment will have to consider the long-running Brexit saga. The uncertainty caused may make it harder for other assets and services to secure investment.

But this uncertainty appears to have increased institutional interest in build-to-rent, given its stable, income driven investment characteristics, and the clear long-term demand for more homes.

Property is a fantastic investment. Twain was right – they aren’t making any more land. What he should have added though was that you need to invest in it in the right way.

Private equity backed businesses saw revenue soar by more than half in the last five years, new data published today shows.

Investment by private equity firms boosted revenue at UK firms by 53 per cent, from £30.7bn in 2013 to £47.1bn last year.

In the last financial year PE-backed companies had a growth rate of 10 per cent, according to analysis of 2,000 firms by accountancy firm BDO

Jamie Austin, head of private equity at BDO, said: “The figures speak for themselves. Businesses that have the backing of private equity investors are driving growth and creating jobs against a backdrop of uncertainty and the UK economy would suffer without them.”

The research showed that private equity backed firms also created on average between five to ten new jobs a year and boosted employment levels by 43 per cent over the five year period, creating an additional 86,500 positions in the UK.

“These businesses are the squeezed middle of the business world. They are too big to benefit from the raft of policies aimed at startups yet too small to have the ear of policymakers like big corporations,” Austin added.

“While successive governments have worked hard to create a business-friendly environment in the UK, there is always more that can be done.

“Fast-growth businesses are the backbone of our economy and should be front and centre of the Government’s post-Brexit thinking.”

British business investment will probably stay weak for the next few years because of uncertainty linked to Brexit, a Bank of England interest-rate setter said, calling into question suggestions of a Brexit deal “dividend” by the finance minister.

As Jonathan Haskel gave his first speech since joining the BoE’s Monetary Policy Committee in September, Prime Minister Theresa May’s Brexit strategy was in meltdown after her failure to win last-minute concessions from the EU ahead of a key parliamentary vote on Tuesday.

Haskel said a planned 21-month transition period that is supposed to come into effect when Britain formally exits the European Union on March 29 might run for longer than expected.

In the longer term, companies also need to know whether Britain will have a customs union agreement with the EU or strike a free trade agreement in order to have a sense of how high any new barriers to trade with the bloc will be, he said.

“The longer-term question is whether investment will eventually bounce back after uncertainty is resolved. The answer to this depends on what trade deal is struck,” he said in a speech at the Department of Economics at the University of Birmingham.

“At least for the next few years the prospect of low investment seems possible.”

Companies in Britain cut back their investment in each of the four calendar quarters of 2018 — the longest such run since the depths of the global financial crisis — as the country approached its departure from the European Union.

PRODUCTIVITY CONCERNS

Haskel said almost 70 percent of the slowdown in business investment in Britain since the Brexit referendum in June 2016 was linked to uncertainty over Brexit.

The BoE is concerned that weak business investment will aggravate Britain’s low productivity growth, holding down growth in wages and making the economy more susceptible to inflation.

With May facing the risk of another humiliating defeat of her Brexit plan in parliament on Tuesday, she has opened up the possibility of a short extension to the current negotiations.

Finance minister Philip Hammond, seeking to help May get parliament behind her deal, has said investment is likely to pick up once companies have more clarity that Britain can avoid an economically damaging no-deal Brexit.

Haskel declined to comment on the implications of weak investment for the BoE’s thinking on interest rates, saying that would be something for his next speech.

“Since this thing… is very hard to predict, that’s the way I would think about it. But that will be the next speech, to trace through the relative impact on the demand and supply,” he said during a question-and-answer session after his speech.

The BoE has said it expects to resume raising interest rates if Britain can seal a deal to avoid a no-deal Brexit.

Governor Mark Carney and some other policymakers have said they think they would probably need to cut rates if Britain fails to secure a transition deal to ease the shock of its exit from the EU.

The UK government hopes that Brexit will make the UK a better place to do business, but new numbers from the Centre for Economic Performance (CEP) show that the opposite is happening. UK firms are voting with their money and offshoring new investments to the rest of the EU.

The study finds that the Brexit vote has led to a 12% increase in new foreign direct investment (FDI) projects by UK firms in EU countries, a total increase in foreign investment of £8.3bn. A no-deal Brexit would further accelerate the outflow of investment from the UK.

This is the first systematic, evidence-based analysis of how the Leave vote has affected outward investment by UK firms. The findings support anecdotal evidence that fears about Brexit are causing UK companies to move investments elsewhere in Europe.

The report, by CEP experts Holger Breinlich, Elsa Leromain, Dennis Novy and Thomas Sampson, found:

The Brexit vote has led to a 12% increase in the number of new investments by UK firms in EU countries.

The estimated increase totals £8.3bn (over the period between the referendum and September 2018). To the extent that increased investment in the EU would otherwise have taken place domestically, this represents lost investment for the UK.

The data show no evidence of a ‘Global Britain’ effect. There has not been an increase in investment by UK firms in OECD countries outside the EU.

Higher outward investment has been accompanied by lower investment into the UK from the EU. The referendum reduced the number of new EU investments in the UK by 11%, amounting to £3.5bn of lost investment. This illustrates how the UK is more exposed to the costs of Brexit than the EU.

The increase in UK investment in the EU comes entirely from higher investment by the services sector. Brexit has not affected foreign investment by UK manufacturing firms. This suggests that firms expect Brexit to increase trade barriers by more for services than for manufacturing, perhaps because the government has prioritised the interests of manufacturing over services in the Brexit negotiations by focusing on reducing customs frictions, while ruling out membership of the EU’s single market.

The report’s findings support the idea that UK firms are offshoring production to the EU because they expect Brexit to increase barriers to trade and migration, making the UK a less attractive place to do business.

Holger Breinlich said, “Our results show that Brexit has already led to an investment outflow from the UK of over £8bn.

“These outflows are likely to accelerate substantially in the event of a no-deal Brexit.”

Dennis Novy said, “The economic risk of Brexit is larger on the UK side of the Channel. British firms feel compelled to invest more in the EU but not the other way around.

“Combined with existing evidence that the Brexit vote has already affected the UK economy through lower real wages, slower GDP growth and fewer firms starting to export to the EU, the initial signs are that ‘Project Fear’ may turn out to have been ‘Project Reality’.”

Thomas Sampson said, “The data show that Brexit has made the UK a less attractive place to invest.

“Lower investment hurts the economy and means that UK workers are going to miss out on new job opportunities.”